Ganesha Ecosphere – Creating Wealth from Waste

About the Company

Incorporated in 1987, Ganesha Ecosphere is engaged in the business of PET (Polyethylene terephthalate) bottle recycling and manufactures Recycled Polyester Staple Fibre (RPSF) and Recycled Polyester Spun Yarn (RPSY). The company has around 20 collections centres for PET on Pan India basis and has manufacturing facilities in Kanpur (Uttar Pradesh), Rudrapur (Uttarakhand), and Bilaspur (Uttar Pradesh). The company has cumulative capacity of 1,08,600 Tonnes per annum of RPSF and yarn. The end-user segment for company’s products is textiles (T-Shirts, body warmers etc.), functional textiles (non-woven air filter fabric, geo textiles, carpets, car upholstery) and fillings (for pillows, duvets, toys). The company currently operates at capacity utilisation of around 90% as per its latest filing. Further, the company has about 25% market share in PET recycling industry and recycles more than 4.92 billion bottles annually.

Brief background on PET recycling industry

Polyethylene terephthalate (PET) provides barrier to oxygen, water, and carbon dioxide and is therefore widely used for carbonated soft drink bottles. PET is also used to make bottles for water, juice, sports drinks, beer, medicines and other wide range of food and consumer products. Therefore, the growth for the end-uder industry is leading to increase in demand and use of PET bottles. In-order to reduce the number of PET bottles ending up in landfills it is essential that all countries have robust PET recycling process in place.

The market size of PET bottle recycling industry in India is estimated to be Rs 3,500 crore as per various industry reports. Further, India has one of the highest PET recycling rates at around 90% – which is higher than the recycling rates for regions like Japan, Europe and US – as per the Council of Scientific and Industrial Research (CSIR) – National Chemical Laboratory (NCL). Around 60% of India’s PET recycling industry operates in organised segment.

The PET bottles are collected through scrap dealers who employ people to collect, segregate and sort the plastic waste. The local scrap dealers sell it to larger vendors, which act as collections centres for PET recycling players. For more details on global PET and waste recycling industry, please refer to World Bank’s What A Waste Report.

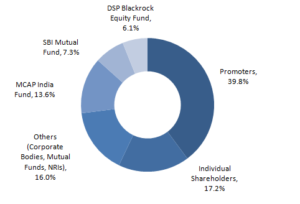

Shareholding Pattern of Ganesha Ecospehere (As of September 2018)

Source: Company Filings

In May 2018, DSP Blackrock Fund invested around Rs 100 crore in the company as growth capital and to reduce long-term debt. The deal led to DSP Blackrock acquiring around 6.1% stake (26,52,520 shares) in the company at a valuation of Rs 377 per share. Other mutual funds which are invested in company are SBI Mutual Fund and Principal Mutual Fund

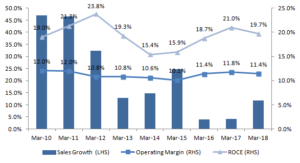

Debt-funded capex followed by equity infusion has supported company’s growth story

The revenue for the company has increased at an impressive 21% CAGR from Rs 135 crore in fiscal 2009 to Rs 754 Crore in fiscal 2018, as the company has consistently undertaken capex to simulate growth. Further, the company has also been able to fairly maintain its margins and return on capital during the period. The company generated 5% of its revenue from exports in fiscal 2018.

Consistent growth in revenue for the company while keeping margins and returns in check

Source: Company Reports

The drop in revenue growth in Fiscal 2016 and 2017 were on account of dip in realisations during the period, as company has to pass on the impact of fall in crude oil prices to consumers.

Though the raw material used by the company does not have direct linkage to crude oil, the price of end product – polyster fiber (manufactued through traditional process using crude oil linked derivatives) is linked to crude oil. Therefore, the company has to pass on impact of low crude oil prices to raw material suppliers in-order to match the prices of its competitors operating in traditional segment or compromise on its margins.

The company has therefore been able to effectively pass on the impact of low crude oil prices, as visible through its margins in fiscal 2016 and fiscal 2017.

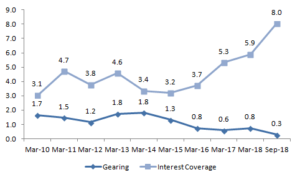

Capital structure improving consistently for company

Source: Company Reports

The gearing for the company dropped from peak of 1.8 in March 2013 to 0.3 in September 2018. The Rs 100 crore infusion through QIP is likely to have aided the drop in long-term borrowings, which was at Rs 65 crore in September 2018 compared to Rs 83 Crore in March 2018. Further, with cash reserves of around Rs 35 crore, the current ratio for the company is also at a decadal high of 2X as of September 2018.

The drop in long-term borrowings will help in reducing the interest costs for the company in March 2019 to the tune of Rs 2-2.5 crore in fiscal 2019 leading to 20-25 bps increase in net profit margins.

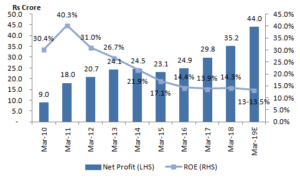

Continous drop in ROE during last ten years

Source: Company Filings

Note: March 2019 profit estimated assuming conservative 5% increase on-year increase in profits in H2 fiscal 2019

The ROE has dropped consistently for the company due to following factors:

- Increase in effective tax rates: The expiry of tax holidays enjoyed by the company in various facilities impacted the -bottom-line for the company. The effective tax-rate therefore increased from 14% in fiscal 2009 to around 34% in fiscal 2018

- Rise in interest costs due to debt-funded expansion: The company adopted aggressive debt-funded growth strategy during fiscal 2010 to 2015 leading to higher long term borrowings and interest costs. The interest coverage ratio for the company had also dropped to as low as 3.2 in fiscal 2015.

- Equity infusion through QIP in August 2018: The investment of Rs 100 crore through QIP route in August 2018 will also have a short-term on the returns ratio for the company, as the reserves will witness sudden jump. However, over the long-run, the reduction in debt will act as a tailwind to overall returns

Company’s Credit Rating enhanced in August 2018

CARE Ratings revised the company’s rating on long-term bank facilities from CARE A- to CARE A in August 2018 which was on account of successful execution of QIP issue of Rs 100 crore leading to more favourable capital structure and also due to company’s expansion plans. For more details, please refer to full credit rating report.

The company’s improved credit rating will also help it offset the rise in the interest rate due to rate hikes announcements by RBI

Road Ahead….

The Company plans to increase its installed capacity for PET Bottle Recycling by 35,000 Tons per annum (TPA) at

green field location, taking the consolidated recycling capacity to 1,43,600 TPA. The estimated investment for the same would be around Rs 250 Crore which would be funded through mix of internal accruals, debt and funds acquired through QIP. As of September 2018, the company has around Rs 35 crore in cash and cash equivalents. Therefore, assuming the company funds a further Rs 75 crore through its CFO (cash flow from operations) in fiscal 2019 and fiscal 2020, it will still have to fund about Rs 140 crore in debt. Therefore, the company continues to be on a growth path and therefore would lead to its balance sheet being leveraged.

The demand from its end-user industry will also remain one of the major keys to company’s growth. Further, the presence and expansion plans of conglomerate like Reliance Industries may also disrupt the overall PET recycling industry.

At Rs 300 per share, the company currently is reasonably valued at 14X FY19E earnings. The company’s ability to execute the impending capex of 35,000 TPA, efficient management of capital structure, growth for domestic textile industry & demand for polyster yarn, and any change in government policy will remain key monitorables for the shareholders going forward.

HAPPY INVESTING!

1 Response Comment