Will DBT in Fertilizer Industry Generate Investment Opportunities?

Introduction: Direct Benefit Transfer

The Direct Benefit Transfer (DBT) was implemented by the Government in January 2013 and has witnessed brisk implementation over last 6 years. The DBT involves transferring the subsidy amount directly to the beneficiaries without any requirement of Government offices to act as intermediaries. The same helps the Government in avoiding leakages and also ensures complete remittance to the target beneficiary. The PAHAL scheme (LPG subsidy) and payments under MGNREGA have been the two successful use-cases of DBT.

DBT implementation in fertilizer industry still in pilot stage

Though the Government has witnessed significant success in implementation of DBT in different segments, the effective implementation in the fertilizer sector still remains a major challenge for the Government. The dynamics of the sector are different as compared to other sectors which has led to delay in its implementation. The subsidy amount to be paid will vary across the beneficiaries/farmers, unlike LPG and MGNREGA where the subsidies provided are fixed. The Government will therefore have to setup data infrastructure to calculate the subsidy due to each of the farmers. The data required for the same will be as follows:

Usage pattern of fertilizer:

The application of fertilizer depends on factors such as crops sown, fertility of land and other demographic factors. The Government will therefore have to collate the required data in-order to track the ideal fertilizer usage and put a land-wise cap on the subsidy. The Government has already started groundwork by accumulating data from PM-KISAN scheme.

Distribution of soil health cards and setting up soil health laboratories

The Government is already in advanced stage in this process and has distributed around 15 crore soil health cards. Distribution of soil health cards will help in balanced application of fertilizers (India’s fertilizer consumption is heavily skewed towards Urea) thereby leading to better yields and prevent over-usage of urea.

Details of land ownership and farmer tenants

It is important that cultivators get the subsidy and not the land-owners who have no exposure to the crop production. Therefore, the Government will have to collate the data of farmer tenants and their relevant details to ensure subsidy amount reached the right target farmer.

Current State of Direct Benefit Transfer in Fertiliser

The pilot DBT in fertilizer sector (Phase-I) was implemented by the Government from 2017 onwards. However, in the current form, the farmers are being sold fertilisers at subsidized cost and subsidy is being transferred to the companies on receipt of sale. This is done as the overall infrastructure is not yet ready to transfer of subsidy directly to farmers.

The PoS (Point-of -Sale) machines have already been installed across the fertiliser retail outlets in the country. Whenever there is a sale to the farmer, the same is recorded on the PoS machine and communicated to the DoF (Department of Fertilizers). The DoF releases the subsidy to the company in around 3 weeks (ideal scenario) from the date of sale. Though this process cannot be ideally called “DBT” (as subsidy is not transferred directly to the beneficiary), the Government documents it as so, since this is the first phase of implementation. Eventually, as the infrastructure would be developed, the Government would transfer subsidy directly to farmers.

How is the current DBT regime different than previous process of subsidy payment

Before 2016 as well, the Government transferred the subsidy directly to the companies. However, the sale of fertilizer was recorded at wholesaler level and not retailer level. Therefore, post the sale to the wholesaler, the company would be paid 85% (95% in case of urea) of the eligible subsidy. The balance 15% (5% in Urea) was released on the confirmation of receipt by retailers in mobile Fertilizer Monitoring System (mFMS). The companies witnessed substantial delay especially in the receipt of 15% of the subsidy as the process was not streamlined.

The current DBT process weeds out these issues as the entire process is tracked through PoS.

Since, the tracking was weak post wholesaler level, there was scope for diversion of fertilizer for industrial use and also in many case across the border leading to losses to exchequer. This would lead to swelling up of Government’s subsidy bill (especially in urea) and thereby delay in payments impacting companies working capital cycles.

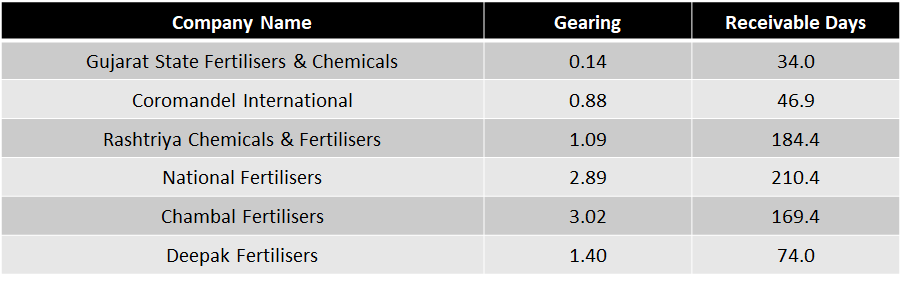

Balance Sheet Strength and Receivable Days for Players (Fiscal 2019)

Also, due to inadequate allotment during many fiscals, the Government provided special banking arrangement to the company, wherein they can avail working capital loans from banks against subsidy receivables

High working capital cycles impacted valuations

The high receivable days on account of delay in subsidy payments by Government led to high interest costs for the players, thereby impacting profitability. Further, the same also led to leveraged balance sheet for most players, as indicated in the table above. On the other hand, the modest rise in rural income has also not aided demand for the players. Therefore, most of the fertilizer companies do not attract premium valuations.

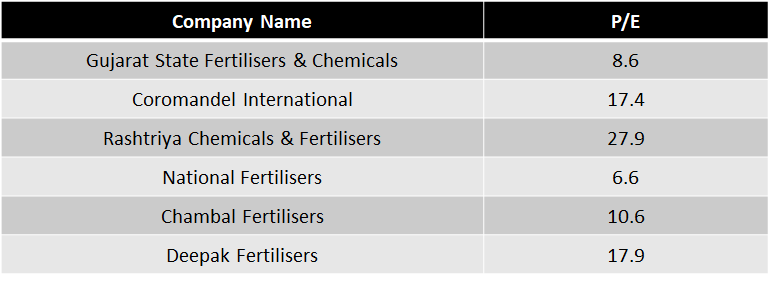

Earning Multiples (Based on Fiscal 2019 earnings)

The premium valuation for Coromandel International is on account of its diversified portfolio and non-subsidy based portfolio. Further, the company has better working capital cycles than most other players in the industry, as indicated in table above.

Also, with some of the companies in the set being state-run, it is also one of the contributing factors to lower earning multiples

The next phase of DBT implementation likely to improve liquidity and demand of non-urea fertilizers

In the next phase of DBT implementation, the Government will transfer the subsidy amount directly to farmer’s account. This will lead to following benefit to the companies:

Receivable days to improve for the players on account of 100% payment by farmers during sale

The Government cannot delay the payment of subsidy to farmers (unlike to companies) on account of various reasons including political; this will help in improving payment cycles for companies

Application of fertilizers to be more balanced due to Soil Health Cards and upfront subsidy payment to farmers, thereby aiding demand for non-urea fertilizers

In the current regime, the usage of urea is significantly higher than global average due to its fixed MRP at around INR 5400/- per tonne as compared to DAP at around INR 24,000/- per tonne.

The upfront payment of subsidy to farmers and distribution of soil health cards will lead to efficient application of fertilizers by the farmers, thereby aiding yields

Therefore, the DBT implementation will aid in improving working capital cycle and likely provide velocity to sale of non-urea fertilizers. Further, stronger balance sheets and reduced finance costs may also lead to revaluation of earnings multiples for some players in the industry. Also, the strong focus of Government to double farm income by 2022, may also provide fillip to growth of sector

Stocks to watch out (Detailed analysis in further posts)

Gujarat State Fertilizers & Chemicals

GSFC is a public sector company promoted by the Government of Gujarat, through its undertaking Gujarat State Investment Ltd (GSIL). As of March 2019, GSIL held 37.84% stake in the company.

- As of fiscal 2019, the company generated revenue of INR 8,598.2 Crore

- Fertilizer segment contributed 74.4% to the total revenue and industrial products constituted the rest

- In terms of profitability, industrial products segment had significantly higher share at 57% to operating profit suggesting higher margins

- Further, during the year the company also started production of Melamine (industrial segment) in a bid to diversify its portfolio. The company is the only manufacturer of the product in the country

- The Gearing for the company as of March 2019 was 0.14X

The high share of industrial products segment to company’s revenue has led to better working capital cycle for the company as compared to peer set, as there is no subsidy component involved. Further, the margins enjoyed by the company is also higher in the segment, as there is no price regulation.

The company also has planned capital expenditure of INR 800 Crore for backward integration and setting up plant for manufacture of MMA (Methyl Methacrylate) at Dahej.

With an EPS of INR 12 per share in fiscal 2019, the company is currently trading at 8.6X.

Coromandel International

Coromandel International, part of Murugappa group, has presence in fertilizer, specialty nutrients and crop protection business. It is the second largest phosphatic fertiliser manufacturer and largest SSP player in the country. The company majorly has its presence in Andhra Pradesh, Telangana, Karnataka and Maharashtra.

As of fiscal 2019, the company recorded revenue of INR 13,260 Crore.

- The company generated around 87% revenue from nutrient (fertilizer) segment and 14% from crop protection segment.

- However, crop protection segment constituted 20% of operating profit, as the company enjoys higher margins in the segment due to no price regulations

- The Gearing for the company was 0.9X in March 2019; the company did not have any long-term debt and only constituted of short-term debt for working capital requirement

The company is undertaking brownfield expansion of the Phosphoric Acid facility at Vishakhapatnam for backward integration.

With an EPS of INR 25 per share in fiscal 2019, the company is currently trading at 17.4X

HAPPY INVESTING!

1 Response Comment