The Indian Pharma Conundrum – Rationalise or push the R&D envelope ?

The turbulent times continued for Indian Pharma space in Q2 FY19. The performance in the regulated markets of US and Europe continued to be a drag for majority of players as pricing pressure and lower new product launches continuing to be a headwind. Though the street is well aware about the narrative on margin pressure in regulated markets, the rationalizing of product portfolio and R&D spends have been the additional highlights in past few quarters. Over the last few years, the Indian Pharmaceutical players have done well to ramp up its R&D spends, which was a necessity rather than a choice in-order to diversify the portfolio and stay abrupt with global trends. However, the continuing pressure on existing portfolio in regulated markets, cues from already launched specialty products (branded generics, complex molecules and biosimilars) by global generic players, rising Chinese API prices may perhaps lead to many players re-aligning their strategy in the short-run.

Global Generics Industry Scenario

The global generics industry constituted around 11% of the overall pharmaceuticals industry as of 2017, as per various industry reports. Further, the share of conventional pharma is expected to drop from 75% in 2017 to 69% in 2024 as biotechnology further strengthens its footing in the global pharmaceuticals industry

The patent cliff reached its peak during 2012 to 2014 – with drugs worth around $110-115 billion going off patent – aiding the increase in the share of the generics segment. Therefore, the global generic players reported healthy margins in this cycle. During fiscal 2009 to 2013, the Indian Pharmaceutical exports grew at 17% CAGR aided by blockbuster drugs going off patent and para IV launches.

Post the patent cliff era of 2014, the global generic players were unable to maintain the same velocity in their revenue growth due to lower opportunities to launch high value drugs. Further, the pricing pressure in generic segment increased significantly due to following factors:

- Entry of many smaller players in regulated markets

- Wholesaler level consolidation in the US

- Lower number of solo Para IV approvals

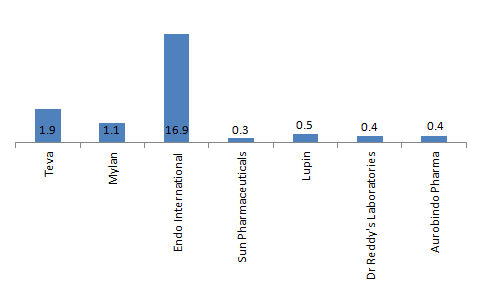

Therefore, with the generic play slowing down and the next patent expiry period due only in 2022, the global generic players looked to diversify their portfolio and build its specialty and biosimilar portfolio through organic as well as inorganic means. This has also had its impact on balance sheet health – The Gearing for Teva – the leading global generic player -increased from 0.65 in 2012 to 1.9 in 2017. Even for Mylan, the total debt increased by 1.8X times during 2014 to 2017, impacting its gearing.

Slowdown in Core business leading to big ticket acquisitions by market leaders

The last few years also witnessed some major M&A transactions by the global generic players. Infact, 2015 – the post patent cliff year – was the year of some of the largest M&A deals in the generic space. Among the major deals in year, Teva acquired Allergan’s generic business in total deal size of around $40.5 billion. Further, Mylan completed acquisition of Abbot Laboratories’ generics business in $5.3 billion deal and Endo International acquired Par Pharmaceuticals – one of the major players in the US generics market – in deal consideration of $8 billion. On the other hand, among Indian counterparts, Sun Pharma acquired Ranbaxy for about $4 billion in 2015 and Lupin acquired Gavis for around $880 million.

Gearing for global generic players and Indian generic players (2017)

Note: For Indian players, gearing is as of March 2018

Source: Company Reports

Therefore, the balance sheets for Indian players are significantly stronger than Global Generic counterparts, as they have been less aggressive in expanding through inorganic means and also in setting up their overall specialty segment machinery in regulated markets. Teva and Endo International generated 60% and 49% of its revenue respectively from specialty segment in 2017. Mylan generated around 20% of its revenue from North America from the specialty segment in 2017. Further, Teva and Mylan have also received approvals from USFDA for their biosimilar launch in US market.

Among Indian players, only Biocon (not a conventional pharma player) – in JV with Mylan – has received approval for launch of biosimilar. Therefore, Indian players lag their major global counterparts in transitioning to different segment

Indian Pharma: Slow and Procrastinated transition away from the Generics

In-line with the global trends post 2014, the Indian Pharmaceutical players also started to ramp up their R&D in specialty, branded and complex molecule space albeit at a slower pace. Some players also actively pursued inorganic opportunities to hasten their foray in the specialty segment. For example –

- Sun Pharma acquired Ocular Technologies to gain worldwide rights for marketing of Seciera (treatment of dry eye diease) and also acquired of Odomzo (branded oncology product) from Novartis in December 2016

- In January 2017, Zydus Cadila acquired Sentynl Therapeutics – a US based specialty pharmaceutical company involved in marketing of pain management related products

- In October 2017 Lupin acquired Symbiomix Therapeutics giving it access to branded Solosec franchise in US market.

However, the acquisitions are yet to bear any material fruits on the company’s financials. As of fiscal 2018, the revenue from specialty segment continued to be very low and generics continued to be business driver. Therefore, there is need for players to push the specialty play for the long-run.

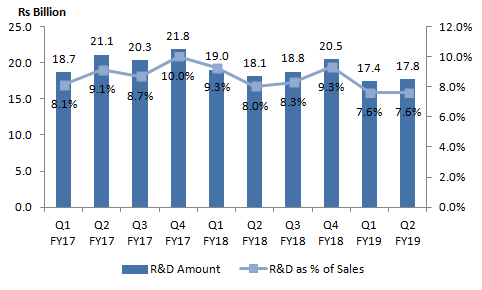

R&D spends in Q2 fiscal 2019 at 10 quarter low for leading players

In the current scenario of continuous pricing pressure on generics and pressing need to push specialty segment, pushing R&D envelope or inorganic acquisitions for specialty segment looks to be the only way forward for Indian Pharmaceutical players. However, over the last 3 quarters the R&D investments for the players has seen some decline. In fact, the cummulative R&D spends in Q2 fiscal 2019 of 5 leading industry players were the lowest in last 10 quarters.

The players are looking to rationalise their R&D spends and also pulling out from products where they believe pricing pressure would be substantial. The current challenging business environment perhaps also has led to this decision, as the companies have to deal with continuous pricing pressure in regulated markets. Further, the rise in prices of Chinese API prices over last few months may also impact the margins in domestic market during H2 fiscal 2019, thereby further impacting cash flows.

Source: Company Reports

Note: Companies Considered: Sun Pharma, Lupin, Cipla, Aurobindo Pharma, Dr Reddy’s Laboratories; quarterly data for few other major players not available in public domain

Therefore, even as Indian Pharmaceutical players navigate through this challenging time and period of margin compression, it will be vital for them to continue to press the R&D button to build a robust long-term business model. Further, alongwith developing their specialty portfolio, the players will also have to strengthen their salesforce in regulated market which would lead to significant upfront costs as well. Currently, the commentary suggests some players are taking a pause before deciding on magnitude of transition it will undertake going forward.

The road ahead certainly won’t be an easy one, as Indian Pharma will have to tread into unchartered territories. Margin pressure and balance sheet strength might be the difficult pills the Indian players will need to swallow for the short-run in-order to have healthy business model over the long-run.

online casino Pin Up https://pin-up-casino777.ru онлайн казино Пин Ап Официальный сайт