Coromandel International – Best Play in India’s evolving Fertiliser Story?

Coromandel International Limited (“CIL”) is in the business of Fertilizers, Specialty Nutrients and Crop Protection. The Company manufactures a wide range of fertilizers in the non-urea (also called complex fertilisers) segment with major presence in Andhra Pradesh and Telangana. The company markets the products through brand “GROMOR”. The Crop Protection business produces insecticides, fungicides and herbicides and markets these products in India and across the globe. On the retail business front, the company has set up around 800 rural retail centers in the States of Andhra Pradesh, Telangana, Karnataka and Maharashtra.

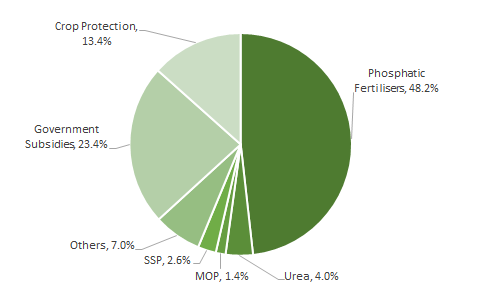

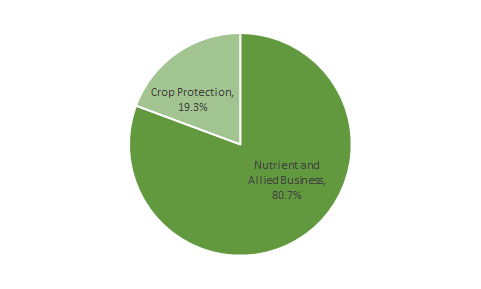

Product-wise revenue share (As of fiscal 2019)

Source: Company Filings

- CIL generates major portion of its revenue from Phosphatic fertilisers (knows as non-urea or complex fertilizers); the retail price of phosphatic fertiliser is not controlled by the Government unlike Urea, where Government decides the MRP

- However, the Government monitors the prices on continuous basis in-order to ensure fair pricing of the fertilizer; in-order to make the non-urea fertilizers more affordable, the Government provides nutrient-based subsidy.

- The nutrient-based subsidy is much lower than the subsidy provided on urea sales

- Therefore, the dependency on Government subsidy receivables is much lower for non-urea manufacturers as compared to urea-manufacturers

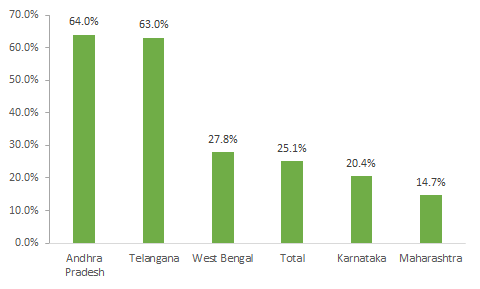

Share in NPK Complexes across major states

Source: mFMS

- CIL has major presence in Andhra Pradesh and Telangana in Complex fertilizer segment with 64% and 63% share respectively in these states

- On Pan-India basis, the company has 25% share in Complex fertilizer segment

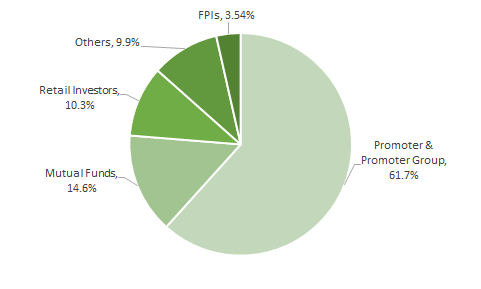

Shareholding Pattern (As of December 2019)

Source: BSE

- EID Parry India (Murugappa Group Company) owns 60.5% stake in the company

- The company has high mutual fund holding at 14.6%; the mutual fund holding increased by 600 bps for the company compared to December 2017

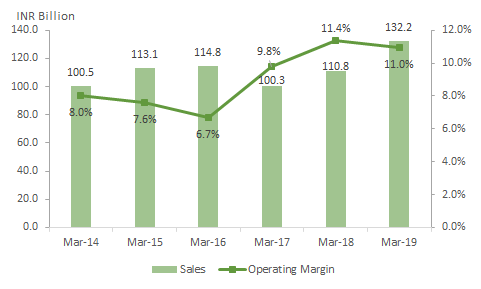

Trend in Revenue and Operating Margin

Source: Company Filings

- The revenue for the company grew at 5.6% CAGR during fiscal 2014 to fiscal 2019 supported by the strong growth in crop protection business

- Further, the margin improvement for the company was aided by crop protection business and phosphatic fertilisers segment (part of Nutrient and Allied Business)

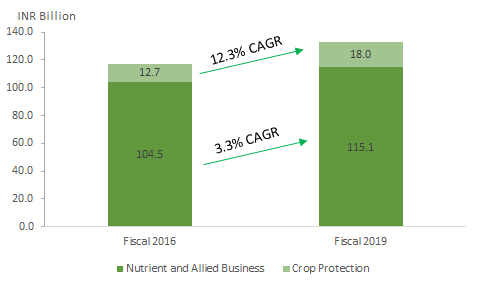

Trend in Segment Revenue

- The business from fertilizers, Specialty Nutrients and Retail business are all included under Nutrients and Allied Business’ segment

- The Crop Protection business recorded a strong 12.3% CAGR growth during the 3-years ending fiscal 2019

- The higher share of crop protection business in the revenue mix also aided profitability for the company, as the business enjoys higher margins compared to the regulated nutrient and allied business segment

Segment-wise share in Profit

Source: Company Filings

- The operating margins for Nutrient and Allied Business was 10.3% in fiscal 2019; for Crop Protection business the margins were 15.7%

- Higher profitability from the Crop Protection business is very crucial to the company’s cashflow as there is no ‘subsidy component’ in the realizations in this segment

- The delay in subsidy payment by Government in Nutrient and Allied Business increases the company’s working capital requirement

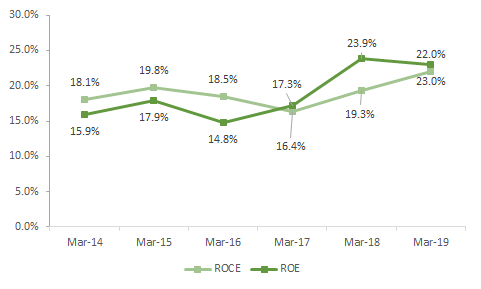

Trend in Return Ratios

Source: Company Filings

- The ROE for the company has improved from 15.9% in fiscal 2014 to 22% in fiscal 2019

- The profitability for the company dipped in fiscal 2016, as the country witnessed 14% below average (long-period average) monsoon in 2015

- Similarly, the country also recorded 9% below-average monsoon in 2018, however the company was able to sustain its profitability during fiscal 2019

- The above-average monsoon in 2019 gave a boost to company’s profitability during fiscal 2020.

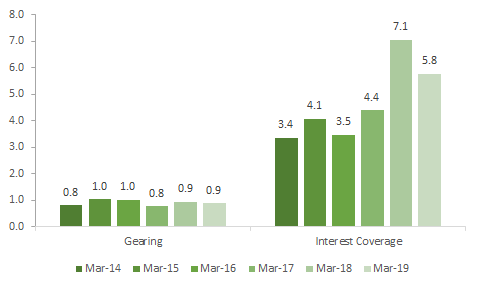

Trend on Gearing and Interest Coverage

- The company’s entire debt is in the form of short-term borrowings for meeting the working capital requirements; the company does not have any long-term debt

- The short-term debt therefore majorly depends on the payment of subsidy by the Government

- To be sure, as of March 2019 the subsidy receivable from the Government was INR 2,393.5 Crore and company’s short term borrowings were INR 2,956.9 Crore

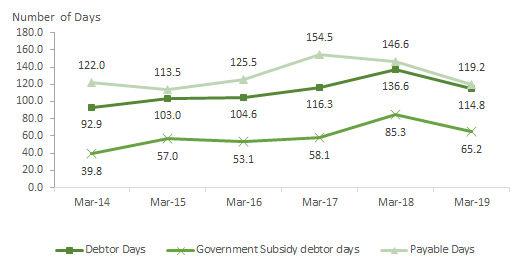

Trend in Working Capital Ratios

Source: Company Filings

- The delay in Government subsidy payable leads to higher debtor days for the company; however, the same is significantly better for the company as compared to its peers

- However, the payable days are higher than the debtors days for the company providing some relief on liquidity requirement

Related Party Transactions

- Payment of INR 6.6 Crore to Parent company (EID Parry Limited) under “Expenses – reimbursed”

- The company did not have any other flags in its related party transactions

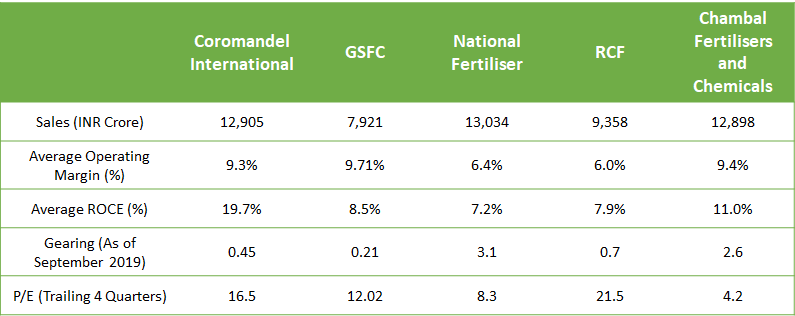

Peer Comparison

Source: Screener, Company Filings

- Coromandal International enjoys premium valuations in the industry on account of substantially higher ROCE as compared to its peers

- This is largely on account of better working capital management and lower share of revenue from highly-subsidised product – urea

- However, GSFC enjoys the strongest balance sheet in the industry; GSFC also has strong presence in the industrial products segment and leadership in melamine market

Key Risks

- The profitability of the company is exposed to the vagaries of the nature; a lower than average monsoon for two consecutive years may put substantial pressure on company’s balance sheet

- The rise in debtor days due to to delay in Government subsidy will lead to increase in short-term borrowings thereby increasing interest cost for the company

- The pressure on Government finances in fiscal 2020 due to current Covid-19 pandemic may lead to delay in payment of Government subsidy thereby increasing interest cost for the company

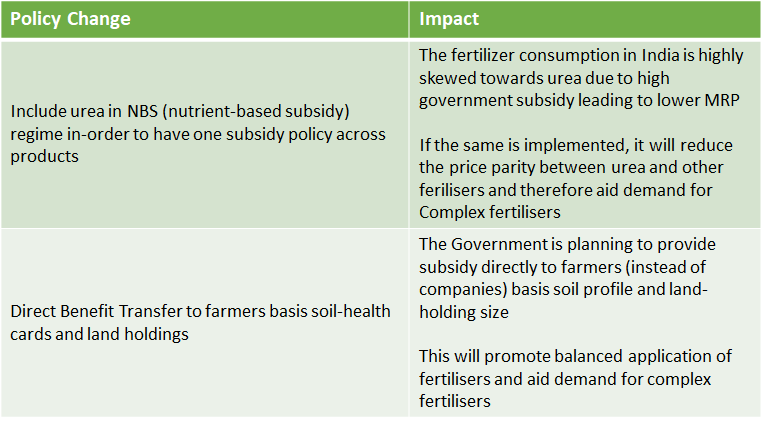

Impact of Policy Changes

The Government has also taken initiatives such as distribution of soil-health cards, sale of fertilisers through PoS machines in-order to track the fertiliser consumption pattern, promote balanced fertiliser application and ensure no slippages in the subsidy paid. Please refer to our previous blog for more details.

Further, new schemes such as PM-KISAN will also provide support to rural consumption over the long-run.

Conclusion

CIL is one of the better managed companies in the capital-intensive fertiliser industry. The company has developed a portfolio of products which reduces its dependence on Government subsidy as compared to its peers. The growth in the crop protection segment (relatively low working capital intensive compared to fertiliser) provides further strength to its cash flows. The company therefore forms a very strong play in India’s agriculture and rural sector growth.

On the demand-side, the company enjoys high stickiness on volume front even in a scenario of lower than average monsoon; however, the realizations take a hit due to lower acreage and yields.

As of April 15, 2020 , the company traded at premium of 16.6X basis previous four quarter earnings.

CIL maybe a major beneficiary of Government’s focus on rural development schemes and reforms in the fertiliser industry.

HAPPY INVESTING!